Choosing the right home for your retirement savings is as important as saving for retirement in the first place. Your retirement plan dictates how much you can contribute annually, how it's taxed, how withdrawals work, what you can invest in, and how much you pay in fees.

Loading paragraph...

Loading image...

Loading paragraph...

Loading table...

Loading paragraph...

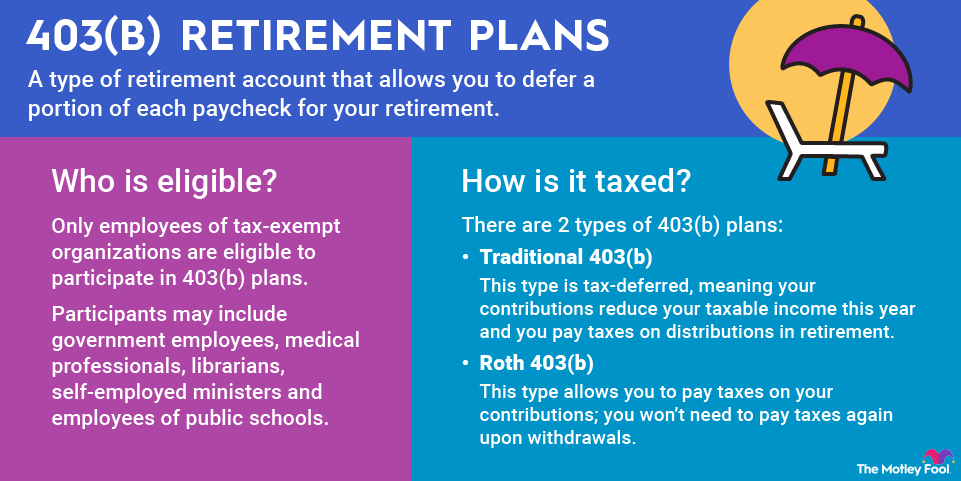

Other employer-sponsored retirement plans

403(b) and 457 plans are other types of employer-sponsored retirement plans you may come across.

Loading hub_pages...

Loading paragraph...

The greater variety of options, coupled with the fact that you can open an IRA with any broker, means you may be able to keep your fees lower with an IRA than you could with the plans listed above.

Loading table...

Loading paragraph...

Loading paragraph...

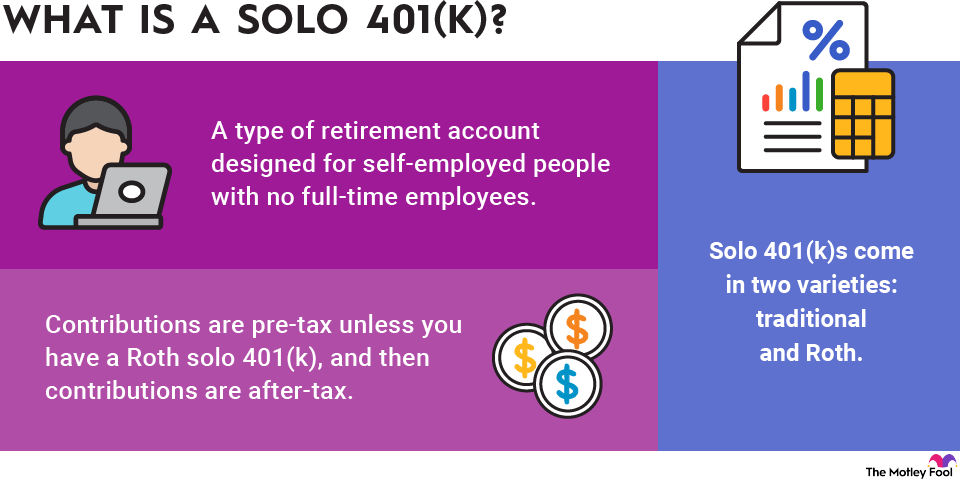

Retirement plans for the self-employed and small business owners

Loading paragraph...

Loading hub_pages...

Loading paragraph...

Loading expert_qa...

Loading faq...

About the Author

Robin Hartill, CFP, is a contributing writer at The Motley Fool. Robin’s work has also been published by Yahoo Finance, USA Today, and Penny Hoarder. She is a graduate of the University of Florida.

The Motley Fool has a disclosure policy.