Bond investment strategies

There are two primary bond investment strategies: active and passive.

Similar to active vs. passive investing in the stock market, active investing seeks to outperform a bond market index by buying and selling bonds based on analysis of market trends, interest rates, and the underlying business.

You can outperform the market with this type of actively managed strategy, but it's more work and is often harder to outperform the index than it looks.

With a passive bond investing strategy, investors typically buy and hold bonds until maturity, aiming to match the performance index. By holding until maturity, you eliminate the risk of fluctuations in bond prices.

For investors looking for fixed income, this is generally a better strategy than active trading.

Bond market vs. stock market

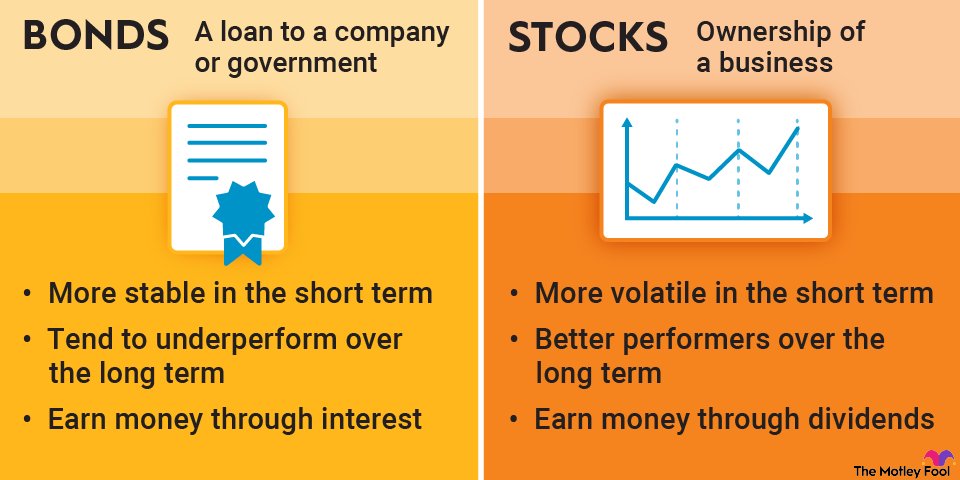

The stock market and bond market represent the two main ways businesses raise cash: through equity or debt. Both stocks and bonds offer investors the opportunity to receive recurring payments. In stocks, these are called dividends; with bonds, they're coupons.

However, with bonds, the purpose of investing is generally to collect the coupon, although investors will be repaid the bond's principal when it reaches maturity. Some stocks pay dividends, but the price of a stock is generally much more volatile than that of a bond, so stock investors usually get most of their return from price appreciation rather than dividends.

The bond market and stock market also influence each other. Higher interest rates tend to make bonds more attractive, pulling money out of the stock market and into bonds. The reverse is true in a low-rate environment.

Stocks are generally riskier than bonds, with more upside and downside, so they attract more risk-tolerant investors. Whether you choose to invest in stocks or bonds will likely be determined in part by your time horizon. Financial advisors often recommend a portfolio that shifts from stocks to bonds as the investor approaches retirement. Moving money from stocks to bonds also helps preserve capital, although you lose the opportunity for higher gains.

Why are bond markets generally more stable than stock markets? Stocks represent a share of ownership in a business, so they move with that business's prospects, which can change significantly. A bond, on the other hand, represents a share of the business's debt, whose price can change modestly with interest rates but is generally stable unless investors fear the company may go into bankruptcy.

Fixed income, by definition, is more stable than stocks, whose return is not scheduled the way bonds are.

The bottom line

The bond market offers valuable opportunities for investors seeking fixed-income streams, and investors of any risk tolerance can find a bond that suits them, from Treasuries to junk bonds to emerging-market bonds.

It also gives corporations and governments a way of raising money. A number of companies prefer to raise capital through the debt market rather than by selling new shares and diluting existing shares.

In a falling interest-rate environment, bond yields will fall and prices on existing bonds will rise, which could pressure lenders. Lower yields can also encourage investors to move into the stock market, seeking yield from dividend stocks.

Because bonds offer a fixed-income stream, they are popular with retirees and other investors with shorter time horizons. Although you may choose not to invest in bonds, every investor should understand the relationship between stocks, bonds, and interest rates.