Retirement means freedom from the workplace, but it also means living on a fixed income for an uncertain amount of time. You don't want to run out of money prematurely, so you need a plan to make your nest egg last as long as possible.

Everyone's situation is different, so retirement income strategies will vary. Here are eight common strategies retirees use to get the most out of their nest eggs.

1. Bucket strategy

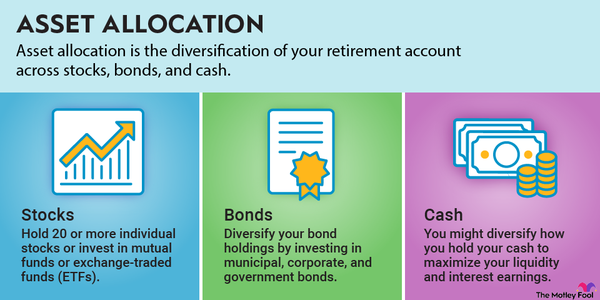

The bucket approach divides your retirement savings into three buckets based on when you'll need to access the funds. Its purpose is to balance investment growth with easy access to your funds. The first bucket is for your emergency fund and money you plan to spend within the next couple of years on living expenses or major purchases. These funds should be kept liquid in a high-yield savings account so you can access them as you need them without worrying about market ups and downs.

The second bucket is for money you plan to use within the next three to 10 years. Place these funds in safer investments, like bonds or certificates of deposit (CDs). As you use up the funds in your first bucket, you can sell or take money out of some of the assets in your second bucket to replenish the first.

The third bucket is for money you don't plan to use for a decade or more. Invest this money in stocks and other assets with greater growth potential. Periodically sell some of these assets and reinvest them in the safer investments you've chosen for your second bucket.

2. Systematic withdrawals

If you’re using the systematic withdrawal approach, you’ll take out a certain percentage of your nest egg in your first year of retirement and increase this amount slightly every year thereafter to counter inflation. One common rule of thumb you may have heard is the 4% rule, which is that you should limit your annual withdrawals to 4% of your nest egg.

It might work in some situations, but it has limitations as well. The 4% rule makes assumptions about how your investments will perform and how long your retirement will last -- and these predictions aren't accurate for everyone. You might need to decrease your withdrawal rate if your investments take a big hit, or you may be able to bump it up if they're performing well. You can use the 4% rule as a starting point, but you should explore a few different scenarios before deciding on the right withdrawal rate for you.

Related Retirement Topics

3. Annuities

An annuity is a contract you make with an insurance company whereby you pay a certain amount of money and in exchange the insurance company sends you guaranteed monthly checks for the rest of your life.

There are several types of annuities, including immediate annuities, with which you give the insurance company a lump sum in exchange for monthly checks starting right away, and deferred annuities, with which you make payments to the company but it does not start paying you for several years.

Annuities can provide another guaranteed source of retirement income besides Social Security, but they're not a good fit for everyone. They can carry high fees and they might not generate returns as large as what you could get from other investments. They can also be difficult to get out of if you change your mind later. Weigh all these factors when deciding if an annuity is a good fit for you.

4. Maximizing Social Security

Social Security provides a guaranteed source of income in retirement, but how much you get depends on your income during your working years and the age when you begin claiming benefits. You must wait to begin benefits until your full retirement age (FRA) -- 66 or 67, depending on birth year -- if you want the full amount you're entitled to based on your work record.

Starting early reduces your per-check benefit. If you begin right away at 62, you'll receive only 70% of your scheduled benefit per check if your FRA is 67 or 75% if your FRA is 66. By contrast, delaying benefits can mean more money over your lifetime, but only if you live a fairly long life. If you delay benefits, you could be eligible for 124% of your scheduled benefit per check at 70 if your FRA is 67 or 132% if your FRA is 66.

5. Earning money in retirement

You can continue to work part-time in retirement to supplement your personal retirement savings. This is a good strategy if you're worried about running out of money prematurely, and it can also help assuage boredom in retirement. If you don't want to work, you could look for alternative ways to earn money in retirement, like buying properties and renting them out or investing in a local business.

Keep in mind that you will owe taxes on these sources of income and that if you don't have a steady paycheck, you must remember to set aside these funds yourself. Consider a designated savings account where you keep money for taxes so you don't accidentally spend it.

6. Tax efficiency

The government taxes different types of savings in different ways, and understanding these is key to holding on to more of your money. You pay regular income taxes on your tax-deferred retirement distributions and no taxes on your Roth IRA and Roth 401(k) retirement distributions, as long as you've had the account for at least five years and are at least 59 1/2 years old. If you have money in a taxable brokerage account, you may owe long-term capital gains taxes on your earnings, but this depends on your income.

You can reduce your taxes by staying mindful of your tax bracket each year and relying more upon Roth savings when you're approaching the top of your bracket. If you have a lower-income year, you could do a Roth conversion to change some of your tax-deferred savings into Roth savings so you won't owe money on those distributions later. You also need to stay mindful of required minimum distributions (RMDs) once you're 73 or older (previously 72) because you could pay a penalty if you don't withdraw enough annually.

7. Health savings account

Health savings accounts (HSAs) are designed primarily for covering medical expenses at all ages, but you can also use them for nonmedical expenses. You'll pay a penalty if you're under 65, but once you pass this milestone, you can use the funds just as you would a traditional IRA’s, with regular taxes on withdrawals, and the added bonuses of tax-free medical withdrawals and no RMDs.

Only those with high-deductible health insurance plans -- ones with a deductible of $1,500 or greater for an individual or $3,000 for families in 2023, up from $1,400 for individuals and $2,800 for families in 2022 -- may contribute to an HSA. Individuals may contribute up to $3,850 in 2023 ($3,650 in 2022), and families may contribute up to $7,750 ($7,300 in 2022).

8. Downsizing

Downsizing reduces your living expenses so your existing savings can go further. You can either move to a smaller home, move to a more affordable area, or both. If you don't want to do that, you might be able to offset some of the cost of your living expenses by renting out extra space.

Personal preference comes into play here, and you must also consider whether it makes financial sense. If home prices have risen in your area since you bought your home, you might not save much money by moving.

The strategies listed here might not all appeal to you, but employing a few can help your retirement savings last a little longer. By taking some time to consider which ones make sense for you, you’ll make the transition into retirement a little smoother.

The Motley Fool has a disclosure policy.