If you have $50,000 or any large amount of money sitting on the sidelines -- maybe in a checking account or a big bank savings account paying little interest -- it's a good idea to put it to work for you. Don't know where to start? Here's some inspiration.

Nine ways to invest $50,000

The prospect of figuring out where to put a significant amount of money can seem scary. So, we put together nine ideas to help you plan your investment strategy.

1. Open a brokerage account

You'll need a brokerage account if you want to invest in stocks, bonds, exchange-traded funds (ETFs), or mutual funds. In a nutshell, a brokerage account is a special type of financial account that allows you to contribute money to buy-and-hold investments.

Buy-and-Hold Strategy

Plenty of excellent brokerage firms offer accounts you can open, and all have slightly different features. Some are rather minimalist and could be ideal for investors simply wanting a place to buy and sell stocks.

Others have features such as sophisticated trading platforms, educational resources, fully functional mobile apps, and much more. The best plan is to compare several top brokerages to see which best meets your needs.

One big tip is that most brokerage platforms will let you test-drive their platforms using some sort of "play money" mode to see if it's right for you.

2. Invest in an IRA

An individual retirement account, or IRA, is a special type of brokerage account designed to help you save and invest for retirement. You can only contribute a certain amount of money each year to an IRA. In 2025, the contribution limits are $7,000 and $8,000, respectively, for those under and over 50 years of age.

This can be a great way to put some of your $50,000 to work. Once contributions are made, money in an IRA can be invested in virtually any stock, bond, or mutual fund you want. There are two main types of IRAs: traditional and Roth IRAs.

A traditional IRA allows you to make tax-deductible contributions, but any withdrawals from the account will be taxable income. Conversely, a Roth IRA doesn't let you deduct your contributions, but qualifying withdrawals will be completely tax-free. It's worth noting that even if you have a retirement plan at work, such as a 401(k), you might still qualify to make IRA contributions.

3. Contribute to a health savings account (HSA)

A health savings account (HSA) is an overlooked investment tool. It is often confused with the other popular tax-advantaged healthcare account, the flexible spending account (FSA), but there are some big differences and things to know:

- Unlike an FSA, money in an HSA can carry over from year to year.

- Contributions are tax-deductible, and money can be withdrawn with no taxes or penalties for qualified healthcare expenses.

- Money in an HSA can be invested, much like money in a 401(k). And tax-free withdrawals for healthcare expenses can be made at any time.

- Once you turn 65, you can withdraw money from your HSA for any reason, although non-healthcare withdrawals are taxable income.

You'll be unable to invest all $50,000 here, as there are annual contribution limits. Even so, an HSA is certainly worth considering if you qualify.

4. Savings account or CD

Savings accounts and certificates of deposit (CDs) can be smart ways to protect your principal. As of late 2025, you can still get a 4% or higher interest rate from these accounts if you do a little research.

Savings Account

The biggest drawback of savings accounts is that interest rates can fluctuate over time. Just because a certain savings account is paying 4% annually now doesn't mean that will be the case next year or even next month.

CDs allow you to lock in your interest rate for a specified period, and they typically pay a bit more than savings accounts. However, you're committing to keeping your money deposited until the CD matures -- or you will pay a penalty.

5. Buy mutual funds

Mutual funds are investments that pool investors' money to buy a portfolio of stocks, bonds, and commodities, among other investments. Mutual funds can be actively managed funds or passive index funds.

In passive index funds, fund managers simply try to match an index's performance. For example, a mutual fund that tracks the S&P 500 invests in the 500 companies in that index to match its performance over time. Alternatively, actively managed mutual funds aim to beat a benchmark index by allowing their managers to choose the fund's investments.

6. Check out ETFs

Exchange-traded funds are similar in nature to mutual funds, except they trade on major stock exchanges. Instead of choosing a specific dollar amount to invest, you choose how many shares of a particular ETF you want to buy.

Most ETFs -- but not all -- are index funds, meaning they aim to match the performance of a specific stock (or bond) index. For example, the Vanguard S&P 500 ETF (VOO -0.11%) should match the performance of the S&P 500 over time.

ETFs, especially index funds, tend to have low investment expenses. This makes them excellent choices for investors building a portfolio from scratch or who simply don't want the risk involved with investing in individual stocks.

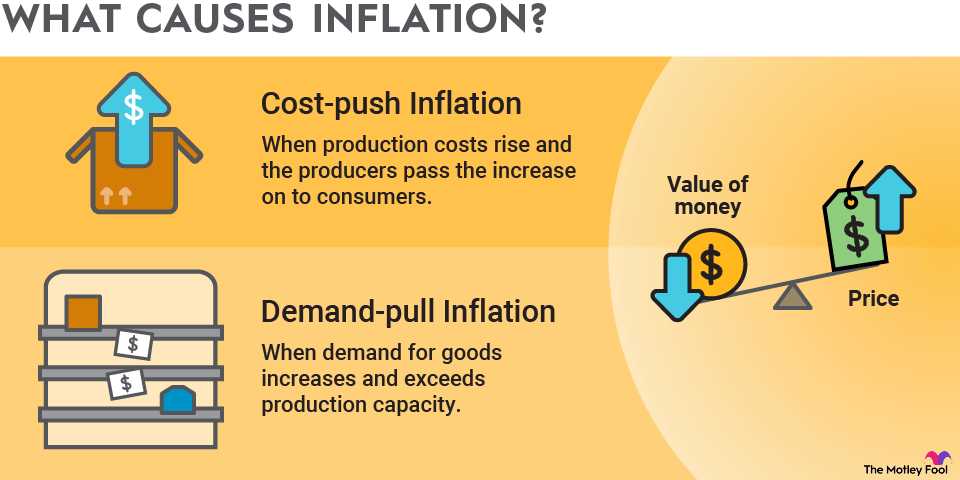

7. Purchase I bonds

One interesting way to invest some of your $50,000 is through Series I savings bonds, commonly known as I bonds. I bonds are a special type of savings bond issued by the U.S. Treasury and designed to protect against inflation.

I bonds pay an interest rate that combines a fixed rate, which stays the same for the life of the bond, and an inflation-based adjustment, which resets every six months. The fixed rate for new bonds issued from May through October 2025 was 1.10%. Including the inflation adjustment, they guarantee a total annualized yield of 3.98% for the first six months.

The main reason we say you could put some of your money to work is that I bond purchases are capped annually at $10,000 per person. And that is one of the main drawbacks of investing in I bonds.

8. Hire a financial planner

Investing can seem overwhelming, especially for people without the time and/or desire to research their choices. If you're in this group, there's nothing wrong with seeking professional help -- but there are some things to know beforehand.

First, know how your financial planner or advisor gets paid. Are they fee-only advisors, or do they make commissions on the products they sell?

Many financial advisors sell high-commission investments, such as insurance products. On the other hand, fee-only advisors make the same fee income regardless of where they invest your money. Fee-based advice is generally the best way to go, but it depends on the particular compensation structure.

Second, make sure your financial planner or advisor is a fiduciary. A fiduciary is required to put your best interests ahead of theirs (this ties back into the high-commission investment products mentioned earlier).

9. Buy a rental property

Being a landlord isn't right for everyone. Even if you hire a property manager, owning rental properties is a more hands-on investment than stocks, ETFs, and most other choices.

That said, real estate investments have significant wealth creation potential. A rental property can generate income, and the property's value is likely to increase over time.

Before you decide to invest in real estate, be sure to do your homework:

- Budget for things like vacancies and maintenance.

- Learn the basics of how to evaluate the potential cash flow of prospective properties.

Those not interested in directly owning and renting a property may want to consider investing in real estate investment trusts (REITs). REITs have consistently outperformed stocks on a 20- to 50-year horizon while representing significantly less volatility than the S&P 500.

Related investing topics

There's no one-size-fits-all approach

An important takeaway is that there isn't an ideal investment strategy or asset allocation that works for everyone. For example, a retired person with $50,000 on the sidelines might want to put it into low-risk income instruments like CDs.

On the other hand, a 30-something with a similar amount of money might want to invest in something with a little more reward potential, such as stocks or real estate. For most investors, the right path might be some combination of the nine strategies listed here.

FAQ

About the Author