Roth IRA rollover rules

Roth IRAs are eligible to receive rollovers from a wide variety of account types, including:

There's no limit to the amount you can roll over, but it must be from another account into a Roth IRA. You cannot roll over in the opposite direction from a Roth IRA into another type of account.

When you roll over funds from a pre-tax account, you'll have to pay income taxes on the previously untaxed amount you roll over. This is considered a conversion.

Roth IRA conversion rules

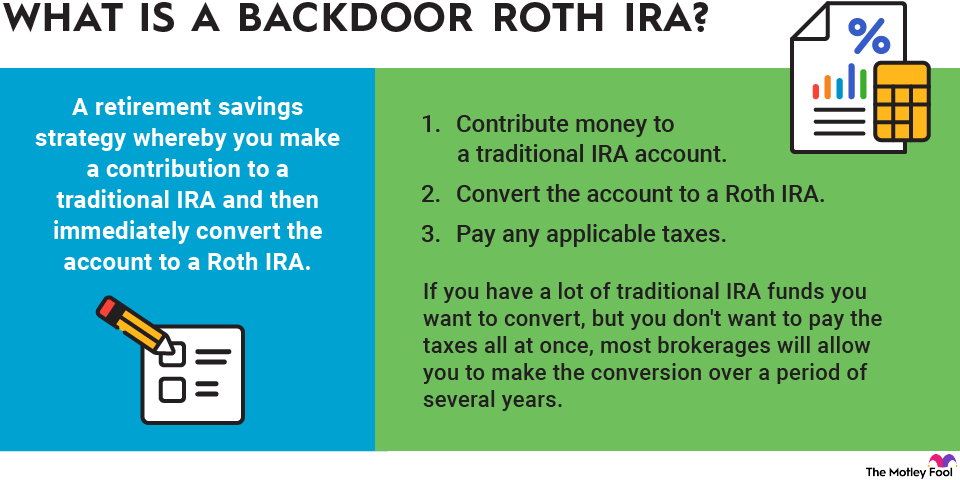

You can convert funds from a traditional IRA or many other pre-tax retirement accounts into a Roth IRA. There's no limit to the amount you can convert; however, doing so requires you to pay income tax on the previously untaxed portion of the funds you're converting.

Roth conversions cannot be recharacterized as traditional IRA funds. This option was eliminated in 2018 by the Tax Cuts and Jobs Act.

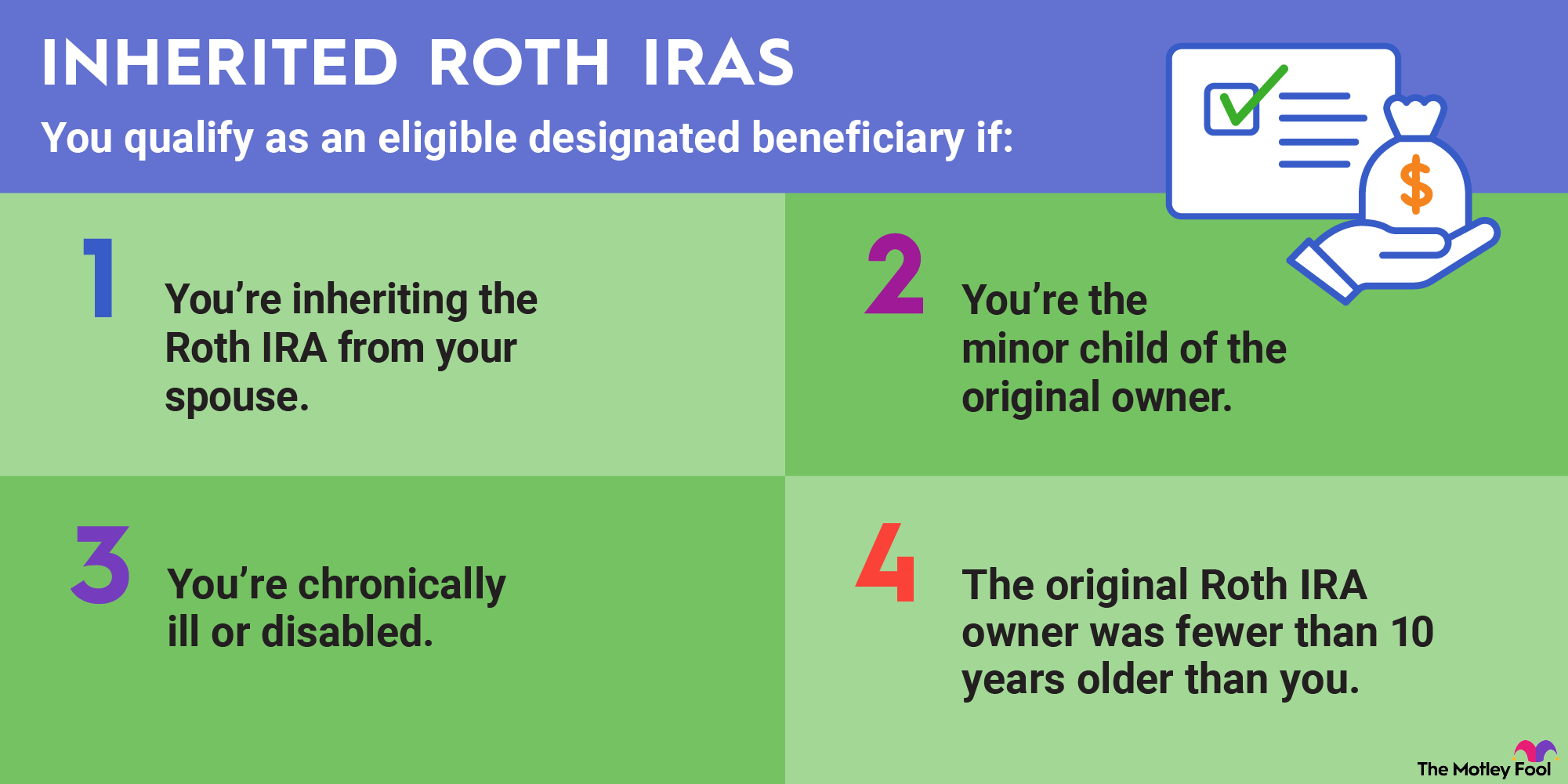

Inherited Roth IRA rules

If you inherit a Roth IRA from your spouse, you have several options:

- Treat the IRA as your own.

- Treat it as an inherited IRA and begin taking required minimum distributions based on your life expectancy beginning the year following the owner's death.

- Treat it as an inherited IRA and deplete the account within five years.

- Take a lump-sum distribution.

If you inherit a Roth IRA from someone other than your spouse, your options have been limited by the 2019 SECURE Act. These beneficiaries may take a lump-sum distribution or cash out the account within 10 years.

Roth IRA transfer rules

When you are transferring Roth IRA funds from one custodian to another, such as in a rollover or conversion, there are two common methods:

- Direct transfer: The assets are transferred directly to the Roth IRA account at your preferred financial institution. This type of transfer can be done in kind, which allows you to keep your existing investments rather than converting them to cash.

- Indirect transfer: You request a check from your custodian and personally deposit the cash in your other Roth IRA. This method is subject to the 60-day rule, meaning you have only 60 days (from the time of fund dispersal to the time of submission to a new account) to transfer your funds tax- and penalty-free. If you fail to complete the transfer within 60 days, you may owe an early withdrawal penalty and income taxes on a portion of it. Additionally, you'll be unable to redeposit the funds into a Roth account beyond your annual contribution limit. Doing so will result in an excess contribution.

Roth IRA trading rules

There are some investments the IRS prohibits you from holding in a Roth IRA:

- Collectibles, including art, rugs, metals, antiques, gems, stamps, coins, alcoholic beverages such as fine wines, and certain other tangible personal property

- Life insurance

The IRS also doesn't allow you to invest borrowed money in your Roth IRA. Therefore, margin accounts are prohibited. Certain options contracts that could require margin borrowing are off-limits, and you're also unable to short-sell stocks.

Other than these restrictions, there's nothing preventing you from day trading in your Roth IRA. Day trading in a Roth IRA protects you from paying taxes on your gains. However, it also means you cannot write off your trading losses -- which is the more likely result for most people attempting to day trade.

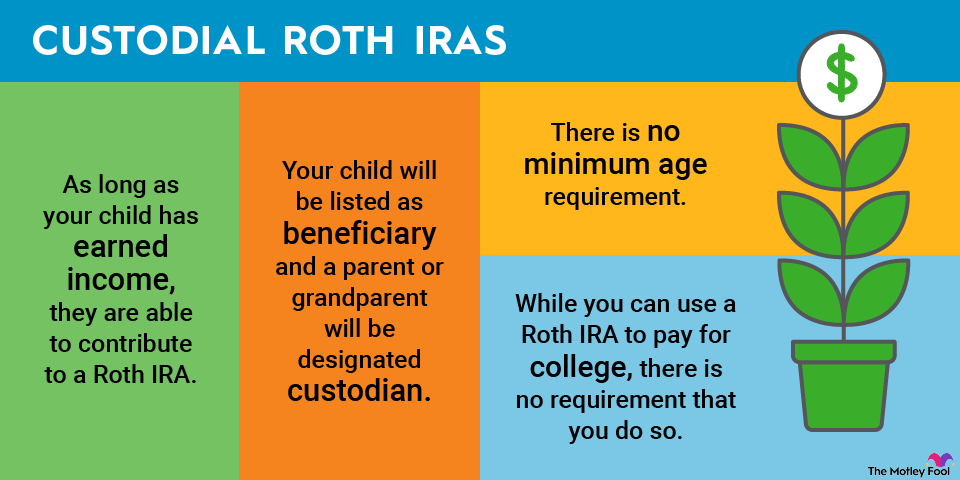

Custodial Roth IRA rules

A custodial Roth IRA allows you to put money away for your child if they earned income. An adult custodian will maintain control of the account for the benefit of the minor until they reach age 18 or 21 (depending on the state they live in). The beneficiary then takes full control of the Roth IRA, converting it into a standard Roth IRA.

Custodial Roth IRAs follow the same rules regarding contribution limits, withdrawals, and trading as regular Roth IRAs.