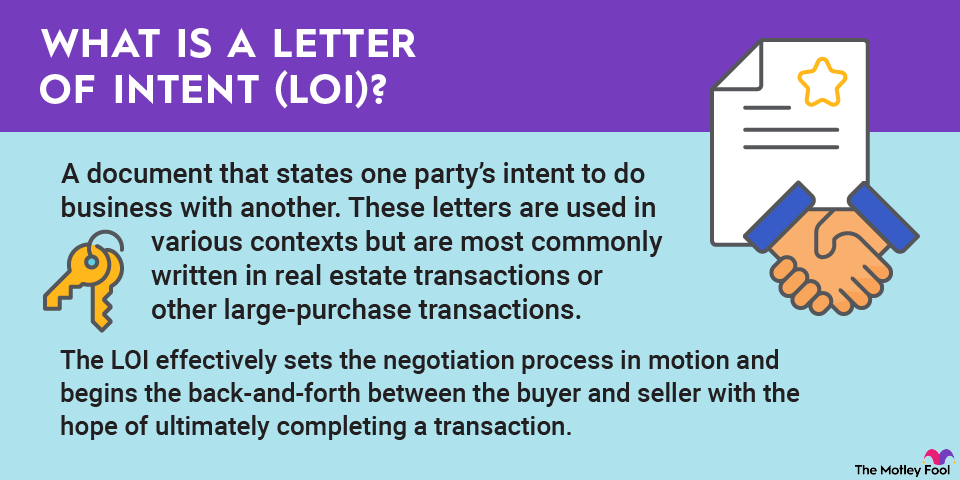

Loading paragraph...

Loading image...

Loading paragraph...

Loading definition...

Loading paragraph...

Loading paragraph...

Loading table...

Loading paragraph...

Loading hub_pages...

Loading paragraph...

About the Author

Nicholas’ investing experience began when he opened up a retirement account shortly after finishing high school. His work experience in financial services began in 2007 in an internship position with a national brokerage firm in Arizona. While his career path led him into civil engineering and related fields, he stayed personally involved and active in the investment realm. He eventually returned to a career in investments and financial services in 2012, running a branch office for the same national brokerage firm, this time just outside of Spokane, WA. During the Great Recession, he began developing a flexible and global investing approach that could evolve with a tumultuous and ever-changing world. Wanting to offer that approach to investment management to his clients paired with a financial planning and consulting business, he founded Concinnus Financial in 2014.

Nicholas grew up in a small town on the Northern California coast just a few minutes from the Oregon border. Growing up in a rainy, quiet little town, he developed a love of music and can play several instruments. He now lives with his wife Kasey and their two Humane Society-rescued dogs. Together they enjoy the outdoors all four seasons of the year, cooking, and craft beer and wine.

Nicholas Rossolillo has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.