Roth IRAs are a powerful tool to build retirement savings. You contribute with after-tax money, and you can make tax-free withdrawals in retirement.

However, only qualified distributions are tax-free. To get the most out of this type of account, you'll need to understand the Roth IRA distribution rules.

Do Roth IRAs have mandatory distributions?

Roth IRAs don't have required minimum distributions (RMDs). You can leave your money in your Roth IRA for as long as you want without needing to make withdrawals.

Most other tax-advantaged retirement accounts, including traditional 401(k)s and IRAs, are subject to RMDs. You need to start withdrawing money at age 73 to avoid penalties. The IRS imposes RMDs because contributions to traditional retirement accounts are made with pretax dollars. This rule doesn't apply to Roth IRAs, since you make after-tax contributions.

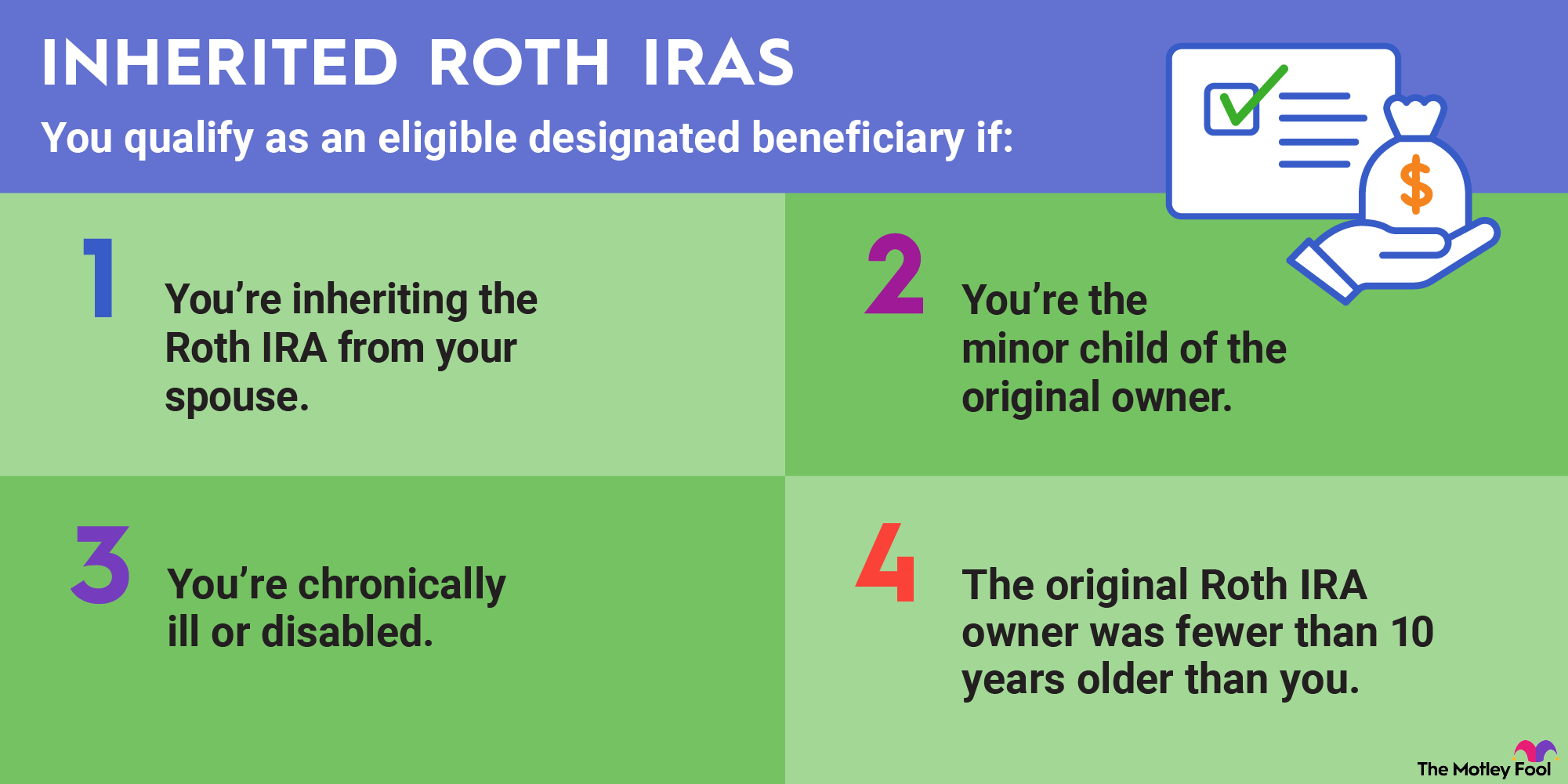

If you inherit a Roth IRA, then it's a different story. Inherited IRAs, whether a traditional or Roth account, have RMDs and require that you liquidate the account within 10 years. There are exceptions if the designated beneficiary is:

- The IRA owner's spouse

- The IRA owner's minor child (the 10-year rule applies once the beneficiary reaches age 21)

- Disabled or chronically ill, by the definition of the IRS

- Not more than 10 years younger than the IRA owner

Can I take an early distribution from my Roth IRA?

You can withdraw your contributed funds from your Roth IRA at any time. Withdrawals of your own contributions are tax-free and penalty-free.

If you withdraw earnings from your Roth IRA before age 59 1/2, those earnings will be subject to taxes and a 10% early withdrawal penalty. There are, however, exceptions to the early withdrawal rules.

You can take distributions before age 59 1/2 without taxes or penalties if you made your first contribution to your Roth IRA at least five years previously and one of the following applies:

- You become disabled under the IRS definition.

- You're withdrawing a maximum of $10,000 to build, buy, or rebuild your first home.

- You die, and the distribution is taken by your heirs.

There are also times when you can avoid the penalty for an early distribution, but not the ordinary income tax on gains. This can happen if:

- You withdraw money to pay unreimbursed medical expenses exceeding a certain percentage of your income.

- You're using the money to pay medical insurance premiums after you've lost your job.

- You're using the funds for qualified educational expenses.

- You're paying back taxes to the government because you are subject to an IRS levy.

The five-year rule for initial Roth IRA contributions

To take tax-free distributions from a Roth IRA, you must wait until at least five years have passed from the time you made your first Roth IRA contribution.

However, the clock doesn't start ticking on the day you put the money into your account. It begins on the first day of the tax year in which you made your contribution. If you make your contribution on April 10, 2026, but designate it as a contribution for the 2025 tax year, then the clock starts ticking on Jan. 1, 2025, and the five-year period ends Jan. 1, 2030.

The five-year rule supersedes other rules. That means that if you have met other requirements, but you didn't make your contribution more than five years ago, you cannot take a tax-free distribution.

The five-year rule for Roth conversions

If you converted a traditional IRA or 401(k) to a Roth account, a different five-year rule applies.

If you withdraw money from a converted traditional account and aren't yet 59 1/2, you will be required to pay a 10% penalty for all early withdrawals. This includes paying the penalty on the amount that was converted, even though you were already taxed on the money when you did the Roth IRA conversion.

The five-year clock applies separately to each new conversion you make. Like the other five-year rule, it starts on Jan. 1 of the year you make the conversion. Unlike with Roth IRA contributions, you can't designate a conversion for the previous year if you make it before the tax filing deadline.

Related retirement topics

Taxes on Roth IRA distributions

If you have met the requirements for a qualified distribution, you will not be taxed on your Roth IRA distributions. You meet these requirements if you are at least 59 1/2 or if you fall into one of the exceptions described earlier, such as if you're withdrawing no more than $10,000 to use toward the cost of your first home.

In all circumstances, you must meet the five-year rule for a distribution to be qualified and enable you to avoid taxes on your distribution.

Remember that if you are taxed on distributions, you will be taxed only on gains. You can withdraw money you contributed to the account tax-free at any time since you made contributions with after-tax funds.

About the Author