Admittedly, it can be challenging to hold a 30-year asset to maturity. For that reason, it's wise to plan your savings bond strategy carefully. Factors to consider include your needs for liquidity and inflation protection as well as your risk tolerance.

Liquidity refers to the relative ease of converting an asset into cash. S&P 500 ETF shares are liquid because you can sell them for cash quickly during regular trading hours. Real estate, on the other hand, is not liquid. It takes time to find a buyer and close the transaction.

Savings bonds have liquidity after 12 months because you can redeem them for cash. But if you intend to maximize your interest, you may prefer to treat savings bonds as illiquid. Once you commit to holding a savings bond until maturity, you assume it won't satisfy any cash needs you have for 30 years.

Inflation protection is offered by I bonds, but not EE bonds. While EE bonds are guaranteed to double in value after 20 years, the interest rate is fixed. The variable rate paid on I bonds is tied to inflation, so it can go up when prices are rising.

Note that interest earned by savings bonds is not paid out regularly. Instead, you receive all accrued interest and outstanding principal when you redeem the bond.

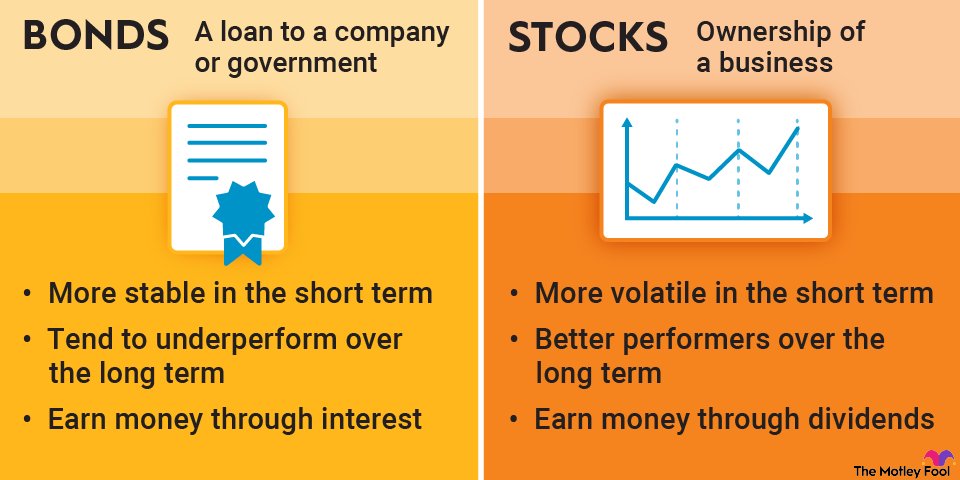

Risk tolerance should always play a role in your savings and investing decisions. U.S. savings bonds have low risk and low returns. If you have a high tolerance for risk, you may prefer a small position in savings bonds or none at all; you might instead focus on more aggressive assets with higher earnings potential. If you want to keep your overall risk low and diversify your net worth, savings bonds could be a good fit.