Investing in growth stocks can be a great way to earn life-changing wealth in the stock market. The key, of course, is to know which growth stocks to buy and when.

Despite increased volatility in the stock market in 2025, growth stocks continue to outperform. The S&P 500 Growth index climbed 21.4% last year. Its counterpart, the S&P 500 Value index, was up just 11%.

However, growth stocks don't always outperform during periods of volatility. In 2022, the S&P 500 Growth index fell 30% for the year, while the S&P 500 index dropped just 19%.

Picking the right growth stock can help you weather the downside while profiting in the long run from its potential. With these tools and strategies, you can position your portfolio for long-term success with growth stocks.

What is a growth stock?

Growth stocks are companies that increase their earnings faster than the average business in their industry or the market as a whole. Often, a growth company has developed an innovative product or service that is gaining share in existing markets, entering new markets, or creating entirely new industries.

The market tends to reward businesses that can grow faster than average for long periods, delivering handsome returns to shareholders in the process. The faster they grow, the bigger the potential returns.

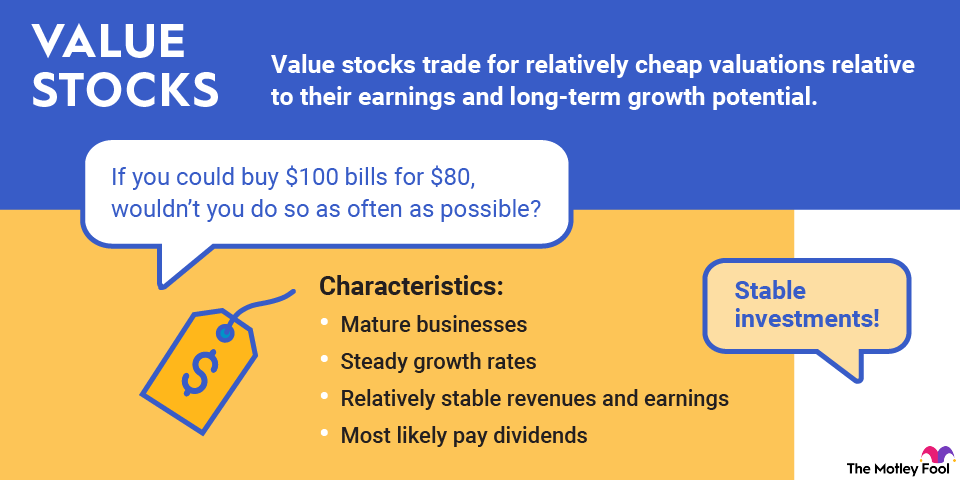

Unlike value stocks, high-growth stocks tend to be more expensive than the average in terms of profitability ratios. Despite their premium price tags, the best growth stocks can still deliver fortune-creating returns to investors. That said, growth stocks can be much more volatile. Big drops in prices may take years to fully recover and catch up with the rest of the market.

High inflation puts pressure on growth stocks because it reduces the future value of their expected earnings. Supply chain constraints also affect the ability of some to expand, and other macroeconomic factors slow the entire economy. However, downturns can give long-term investors a buying opportunity when growth stock prices are low.

Top growth stocks in 2026

To provide you with some examples, here are 10 excellent growth stocks available in the stock market today.

| Company name | Company ticker | Market cap | Industry |

|---|---|---|---|

| Meta Platforms | NASDAQ:META | $1.8 trillion | Interactive Media and Services |

| Shopify | NASDAQ:SHOP | $170.8 billion | IT Services |

| Uber Technologies | NYSE:UBER | $166.3 billion | Road and Rail |

| Block | NYSE:XYZ | $36.7 billion | Diversified Financial Services |

| MercadoLibre | NASDAQ:MELI | $108.9 billion | Multiline Retail |

| Nvidia | NASDAQ:NVDA | $4.6 trillion | Semiconductors and Semiconductor Equipment |

| Netflix | NASDAQ:NFLX | $352.5 billion | Entertainment |

| Amazon | NASDAQ:AMZN | $2.6 trillion | Multiline Retail |

| Salesforce | NYSE:CRM | $198.9 billion | Software |

| Alphabet | NASDAQ:GOOG | $4.1 trillion | Interactive Media and Services |

How to find growth stocks

To find great growth stocks, you'll need to:

- Identify powerful long-term market trends and the companies best positioned to profit from them.

- Narrow your list to businesses with strong competitive advantages.

- Further narrow your list to companies with large addressable markets.

Cloud Computing

FAQ

FAQ: Growth stocks

Expert Q&A on growth stocks

About the Author