There are right and wrong reasons to sell a stock. While it's generally a bad idea to sell a stock simply because its price increased or decreased, other situations perfectly justify placing one or more sell orders.

Let's delve into several good reasons for selling a stock, when to sell stock for a profit or loss, and which circumstances do not justify selling a stock.

Reasons to sell

Reasons to sell a stock

Here's a rundown of five scenarios that can justify selling a stock:

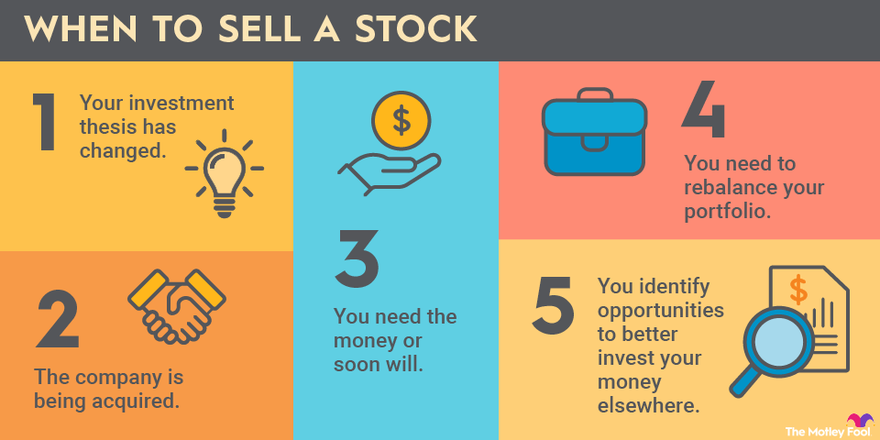

1. Your investment thesis has changed

The reasons why you bought a stock may no longer apply.

Examine why you bought a stock in the first place and ask yourself if those reasons are still valid. You should have a reason -- or an investment thesis -- for each of your stock investments, other than just wanting to make money.

If something fundamental about the company or its stock changes, that can be a good reason to sell. For example:

- The company's market share is falling, perhaps because a competitor is offering a superior product for a lower price.

- Sales growth has noticeably slowed.

- The company's management has changed,

- Managers are making reckless decisions, such as assuming too much debt.

Of course, this list isn't exhaustive. But the point is that if something substantially changes that contradicts your investment thesis, that's one of the best reasons to sell.

2. The company is being acquired

Another potentially good reason to sell is if a company announces it has agreed to be acquired.

After an acquisition is announced, the stock price of the company being acquired typically rises to a level close to the agreed-upon purchase price. Since further upside potential can be quite limited, it may be wise to lock in your gains shortly after the acquisition announcement.

Specifically, the way the company is being acquired affects whether selling your stock is the right decision. A company can be acquired in cash, stock, or a combination of the two:

- For all-cash acquisitions, the stock price typically quickly gravitates toward the acquisition price. But if the deal is not completed, then the company's share price could come crashing back down. It's rarely worth holding on to your shares long after the announcement of an all-cash acquisition.

- For stock or cash-and-stock deals, your decision to hold or sell should be based on whether you have any desire to be a shareholder in the acquiring company. For example, real estate brokerage Redfin (NASDAQ:RDFN) agreed in March 2025 to be acquired by mortgage giant Rocket Companies (RKT -3.15%) in an all-stock deal. Redfin shareholders who didn't want to become Rocket investors would have had a good reason to sell.

3. You need the money, or soon will

It's generally a best practice not to invest in the stock market with any money you expect to need within the next few years. But if you need the money, that's certainly a valid reason to sell.

Perhaps you want to purchase a house and sell some stock to cover the down payment. Or you may have children who plan to attend college in a few years, and you want to convert your stock holdings into more secure investments, such as certificates of deposit (CDs).

4. You need to rebalance your portfolio

Your investment portfolio can become unbalanced in one or more ways. That is why periodically rebalancing your portfolio -- which may involve selling some stock -- is necessary for most investors. These are two of the most common circumstances preceding a stock sale:

- Owning a high-performing stock: If you own shares that have significantly increased in price, your position in the company may represent a large portion of the value of your portfolio. While this is a good problem to have, you may not be comfortable with having so much of your money invested in a single company and choose to sell part of your stock.

- Seeking to reduce your stock exposure: As you get closer to retirement, it's smart to gradually reduce your portfolio's stock holdings in favor of safer investments such as bonds. One popular rule of thumb (known as the Rule of 110) is to subtract your age from 110 to determine the percentage of your portfolio that should be invested in stocks. If your portfolio seems too stock-heavy, then selling some stock to reallocate your resources can be a good decision.

5. You identify opportunities to better invest your money elsewhere

In a perfect world, you'd always have spare cash to invest every time you identify an attractive investment opportunity. Since that's probably not the case, you may decide to sell stock to invest the cash differently.

Let's say you notice an incredible buying opportunity for one of your favorite stocks and decide you want 10% of your portfolio to be allocated to this investment. If you don't happen to have 10% of your portfolio sitting in cash, you may decide to sell some shares of other stocks or exchange-traded funds (ETFs) you own to free up some capital.

Even if there is nothing wrong with the other stock or ETF, recognizing an excellent long-term opportunity elsewhere can be a valid reason to sell.

Just be aware that there's a fine line between selling to take advantage of an opportunity and overtrading.

Selling for profit

When to sell stocks for profit

Any of the above are good reasons to sell a stock for a profit. Having earned a profit from an investment can further justify selling the stock to pay for a major purchase, your living expenses in retirement, or as part of your portfolio allocation strategy.

But don't sell a stock for profit just because the share price has increased. Doing that would be falling into the trap of believing that it's a good idea to "take some money off the table" if a stock gains value.

To be perfectly clear, selling just because a stock went up is a terrible reason.

Selling at a loss

When to sell stocks at a loss

Similarly, it's usually a bad idea to sell a stock only because its price decreased, if none of the reasons listed above apply.

Having said that, selling losing investments (especially if you see better opportunities elsewhere) can help you save money on your taxes. Investment losses can be used to offset capital gains.

As legendary investor Warren Buffett says, "The most important thing to do if you find yourself in a hole is to stop digging." If your original reason for buying a stock no longer applies, or if you were just plain wrong about the company, then selling at a loss rather than continuing to hold may be your best option.

When not to sell

When not to sell a stock

It's important to clearly know when not to sell a stock. Here's a list of some of the situations in which it's inadvisable to sell your shares:

- Don't sell a stock just because its price increased. Winning stocks often increase in price for a reason, and they also tend to keep winning.

- Don't sell a stock just because its price decreased. Every investor wants to buy low and sell high. Selling a stock just because its price fell, if the reasons you bought it still apply, is literally doing the exact opposite.

- Don't sell stock just to save money on taxes. While the tax strategy discussed earlier, which is known as tax loss harvesting, can reduce your taxable capital gains by incurring losses on unprofitable stock positions, it's nonetheless a bad idea to sell stocks just to lower your taxes. Tax loss harvesting can be a smart tax-saving strategy, but only if you are choosing to sell a losing stock for other valid reasons.

Related investing topics

The Motley Fool sells stock regularly, too

While The Motley Fool always approaches investing with a long-term perspective, that doesn't mean we only suggest stocks to buy.

We regularly give "sell" recommendations to our members, often for one of the reasons described above. There can be several valid reasons to sell a stock, and many long-term-focused investors frequently have reasons to offload parts of their holdings.

FAQ

When to sell stocks FAQ

How do you know when to sell your stock?

There are several good reasons to sell a stock, including but not necessarily limited to:

- Your investment thesis has changed.

- The company is being acquired.

- You need the money for a specific purpose.

- You want to rebalance your portfolio.

- You see better investment opportunities elsewhere.

What is the 3-5-7 rule in stocks?

The 3-5-7 rule is a stock trading guideline that says that you should limit risk to 3% of your account balance on any single trade, temporarily pause trading if your account value falls by 5%, and taking a step back and examining your trading strategy if your account falls 7% in a week.

What is the right time to sell stocks?

There's no perfect time to sell stocks, but it can make sense to sell a stock if certain factors apply. These include, but are not limited to, if your investment thesis has changed, the company is being acquired, you need the money, or if you see better investment opportunities elsewhere.

At what percent increase should I sell a stock?

It is generally not a great idea to sell a stock just because it went up. But if a stock is higher and there's another valid reason for selling -- such as needing to rebalance your portfolio -- it could be a good idea to sell some of a winning stock position.